June 2026

Renters insurance covers belongings after theft or disaster

For an average of $20 a month, Texans can buy renters insurance to protect their belongings from theft or damage.

Renters insurance typically includes three types of coverage:

- Personal property coverage: Covers your belongings – even items stolen out of your car or while you’re traveling.

- Additional living expenses: Pays if you have to move while your house is being repaired to fix damages your policy covers.

- Personal liability: Protects you if someone is injured at your place and pays legal costs if you’re found liable and taken to court.

Some landlords might require you to have a renters policy. Make sure the policy you buy will pay to replace your personal property.

Your policy will pay to replace or repair your belongings up to a dollar limit. This is the most the company will pay, even if the cost is higher. Some policies limit payments for certain kinds of property. Common limits are $100 for cash, $2,500 for items used for business, and $500 for jewelry and watches. Ask your agent about buying more coverage for expensive items or collectibles.

Most policies will cover damage from fire, smoke, theft or vandalism, and certain kinds of water damage. They don’t cover flood damage. Visit the National Flood Insurance Program for information about flood coverage.

Have a question about insurance? Call the Texas Department of Insurance at 800-252-3439 or visit www.tdi.texas.gov.

May 2026

Is your house ready for your vacation?

Planning an out-of-town trip? Make sure to prepare your house before you leave, reducing the likelihood of damage that could lead to an insurance claim.

Before heading out, take time to make your home more safe:

Set timers on interior lights. Criminals look for easy targets. Use a timer on a few lights to make it look like someone is home. Also, don’t let packages or mail pile up. Make sure valuables aren’t visible to someone looking through windows, and don’t leave a key outside.

Don’t post on social media. It’s wise not to post online that you’re away even if you think only friends and family can see your social media updates.

Lock doors and windows. This seems obvious, but it’s easy to overlook. Before you leave, walk around the house to make sure everything is locked.

Unplug TVs and computers. You never know when an electrical storm could cause a power surge. To protect expensive electronics, unplug them or plug them into a surge protector.

Turn off the main water supply to your home. Even a minor leak can cause major damage if no one is home to catch it.

Have a question about insurance? Call the Texas Department of Insurance at 800-252-3439 or visit www.tdi.texas.gov.

April 2026

Why you should consider a flood insurance policy

Most homeowners insurance doesn’t cover damage from flooding after a storm.

And no matter where you live, you could face a flood.

Just an inch of floodwater can cause about $25,000 in damage to an average size home. If you don’t have flood insurance, you’ll have to pay for those repairs on your own.

So, consider shopping for a flood policy.

Ask your insurance agent if your home or renters insurance company offers a flood policy.

The other option to buy flood insurance is the National Flood Insurance Program (NFIP). A NFIP policy covers your home for up to $250,000 and up to $100,000 in belongings. Renters can also get NFIP coverage for up to $100,000 in belongings.

With hurricane season starting in June, now is a good time to buy a flood policy. A policy usually starts 30 days after buying it, so don’t wait until a storm’s on the way.

Have a question about insurance? Call the Texas Department of Insurance at 800-252-3439 or visit www.tdi.texas.gov.

March 2026

What to know about insurance and your roof

If bad weather damages your home’s roof, your homeowners insurance can help. It’s important to know how much coverage you have.

When buying or renewing your insurance, ask your company or agent these questions:

- Is my roof info correct? Ask your agent if the age and material of your roof are correct on your policy. Tell your insurance company if you replace your roof so they can update the age.

- How much will my policy pay for roof damage? Some policies pay the full cost of a new roof. Others pay less based on the roof’s age and condition. Many policies reduce coverage based on your roof’s age and materials.

- What’s my deductible? A deductible is what you pay before your company will pay. The deductible for wind and hail damage is often more than for other damage. If it is, you’ll pay more out of pocket to fix your roof.

- Will you cover my roof if it’s in bad shape? Your policy might not pay if your roof is damaged. When you fix or replace your roof, ask your company if they can add roof coverage back to your policy.

- Can I get a discount if I replace my roof? New roofs often get a better rate than older ones. If you replace your roof, consider materials resistant to wind, hail, or fire. Some companies give discounts for roofs with those materials.

- If part of my roof was damaged, will my policy replace the entire roof? Your company might not pay to replace the entire roof, even if the new shingles don’t match the old ones perfectly.

- When should I file a claim? You can file a claim if a storm, tree, or something else damages your roof.

February 2026

Insured Texas drivers have a consumer bill of rights

When you insure your car or truck, you get lots of information—including a Texas consumer bill of rights for auto insurance.

Too much information? Let’s make this easier.

In Texas, you have the right to:

- Call the Texas Department of Insurance (TDI) for information and help with a complaint against an insurance company.

- Choose the repair shop and parts for your vehicle. An insurance company can’t tell you or the body shop what brand, age, vendor, or condition of the parts you can use. They also aren’t required to pay more than a reasonable amount.

- Ask your insurance company about your policy. The company can’t use your questions to determine your premium or deny, non-renew, or cancel your coverage. You can ask questions about your policy, the company's claims filing process, and whether the policy will cover a loss—unless the question is about damage that results in an investigation or claim.

- Dispute the amount of your claim payment or what your policy covers. Contact your insurance company or the body shop. You can also ask an attorney or appraiser to look at the damage.

- Cancel your policy any time and be refunded the remaining premium.

- File a complaint with TDI.

Read the full bill of rights (PDF) on TDI’s website.

Have a question about insurance? Call the Texas Department of Insurance at 800-252-3439 or visit www.tdi.texas.gov.

January 2026

Look at your plan on HealthCare.gov before enrollment ends

The Texas Department of Insurance (TDI) advises Texans with health insurance through HealthCare.gov to log on and look at their plan.

Plans change every year, so the price might be different. If the price isn’t right, you can switch plans until January 15 when open enrollment ends.

TDI has resources to help you shop for coverage and avoid scams.

Some highlights:

- Look at your plan to know how much you’ll pay in premiums, copays, and deductibles.

- If you switch plans, ask if the new plan lets you see your current doctors and covers your medications.

- If you buy a plan on a website other than HealthCare.gov, know what you’re buying. Alternative health plans have fewer benefits and more limits than traditional health insurance.

You can call our Help Line with general questions about insurance at 800-252-3439.

December 2025

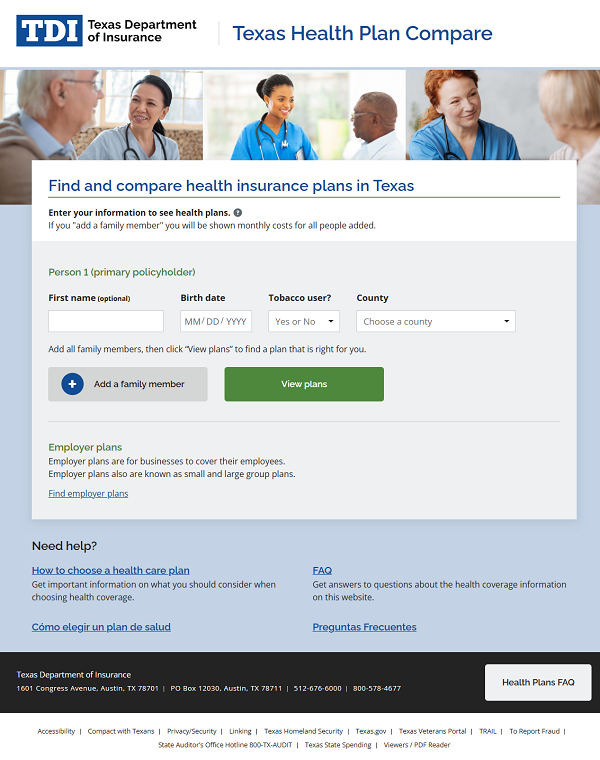

Compare and choose a health plan using Texas Health Plan Compare

Wondering how to pick among Texas health insurance plans?

Say whether you use tobacco and share your birth date and home county, then the Texas Health Plan Compare website lists locally available plans. When you're ready to buy, you can go to Healthcare.gov or buy a plan on your own.

For each plan, you’ll see:

- The company offering the plan, the plan type, and the coverage level.

- The total monthly premium (before any tax credit you might get on HealthCare.gov).

- Your copay amount for a doctor or specialist visit.

- Your deductible; how much you pay up front each year before the plan pitches in.

- The maximum amount you will have to pay out-of-pocket each year for medical services.

- The percentage of complaints people filed about the insurance company.

Next, you can click to compare plans. The results also give you access to each plan’s list of covered drugs and directory of doctors and hospitals.

Ready to roll? Go to the site’s guide to choosing a plan.

Have a question about insurance? Call the Texas Department of Insurance at 800-252-3439 or visit www.tdi.texas.gov.

November 2025

Stop kitchen fires, protect your home

Most home fires start in kitchens.

Learn about preventing and putting out fires:

- Don’t walk away while food is cooking. If you have to leave, even for a short time, turn off the burner.

- If something catches fire on your stove, cover the pan with a lid to smother the flames. Leave the pan covered until it’s cool.

- If the fire is in the oven, turn off the heat and don’t open the door.

- Never pour flour or water on a cooking fire.

- If you have any doubt about fighting a fire, just don’t. Get away by going outdoors. When you leave, close doors behind you to help contain the fire. Call 911 from outside.

September 2025

Outdoor burning: What to know before you light the match

If you plan to light an outdoor fire, check first with your city and county about burn bans and local fire rules. Check the Texas burn ban map to see county burn ban information maintained by the Texas A&M Forest Service.

Statewide, Texas limits outdoor burning to:

- Campfires, bonfires, fire pits, and cooking fires.

- Household trash fires on your home property—only if you don’t have trash pickup.

If you are planning a large outdoor burn, call the Texas Commission on Environmental Quality (TCEQ) at 888-777-3186. TCEQ sets the outdoor burn rules for Texas.

Most wildfires start from carelessness. Control your fire by putting trash, grass, leaves, and branch trimmings in a burn barrel or similar container. Top it with a screen or metal grid.

Also, keep water, a shovel, and a rake handy in case your fire starts to spread. Finally, stay by your fire until it’s out.

Items that shouldn’t go into a fire include aerosol cans or anything that could explode, electrical insulation, and building materials like treated lumber, and plastics and asphalt-based materials.

If you spot a dangerous fire, call 911.

For more information, visit the Texas State Fire Marshal’s Office, a division of the Texas Department of Insurance.

August 2025

Get a CLUE about the insurance history of a home or car

Need more information before you buy that home or car?

Check its insurance history by getting a CLUE report.

What’s the report? It’s the Comprehensive Loss Underwriting Exchange or CLUE report. It shows claims filed for homes and cars for the past seven years. Most Insurance companies report information based on filed claims, including:

- Date of loss.

- Loss type.

- Amount paid on claim.

How do I get a report? If you’re buying a home or car, you can ask the current owner for the report.

Each year, you can get a free report on property you own by contacting LexisNexis. You also can contact LexisNexis to dispute information in the report or to add an explanation.

Have a question about insurance? Call the Texas Department of Insurance at 800-252-3439 or visit www.tdi.texas.gov.

July 2025

Leave July 4 fireworks to the professionals

Love fireworks? To stay safe, let a professional light up your Independence Day.

State Fire Marshal Debra Knight advised: “If you want to see great fireworks, go to a pro show. Our office has issued many permits for communities to enjoy Fourth of July shows. You probably have one nearby.”

Another caution: Your county might be under a burn ban. Most communities don’t allow you to use fireworks within city limits or during burn bans.

Check with your local fire department to see what’s allowed.

“Also, there are no safe fireworks for children,” Knight said. “Some sparklers burn at temperatures of nearly 2,000 degrees, as hot as a blow torch.

“Celebrate,” Knight said, “and stay safe.”

Want to learn more about fireworks safety? Visit the State Fire Marshal’s Office website at www.tdi.texas.gov/fire.

June 2025

Five tips to be ready for a disaster

Everyone wants to be ready for a disaster.

Five easy ways to get started:

- Install a weather app on your phone. Turn on notifications or check it before bad weather to know what’s heading your way.

- Make a list or inventory of the stuff in your house. Email it to yourself or keep it online. Include item model and serial numbers. Take photos or videos of each room in your house, including closets and drawers. When you need to file a claim, the list and photos will help.

- Pack a “go kit” of supplies you can take with you if you need to leave in a hurry. Include water, food, clothes, chargers, medicines, and pet supplies. Have copies of your home, auto, and health insurance cards.

- Consider buying flood insurance. Most home insurance policies don’t cover flood damage; you’ll need a separate flood policy. Flood policies often have a 30-day waiting period before taking effect.

- Check that your insurance policies are up to date and provide enough coverage. Your coverage limits might be too low if you’ve built onto your house or bought furniture or electronics.

Have a question about insurance? Call the Texas Department of Insurance at 800-252-3439 or visit www.tdi.texas.gov.

May 2025

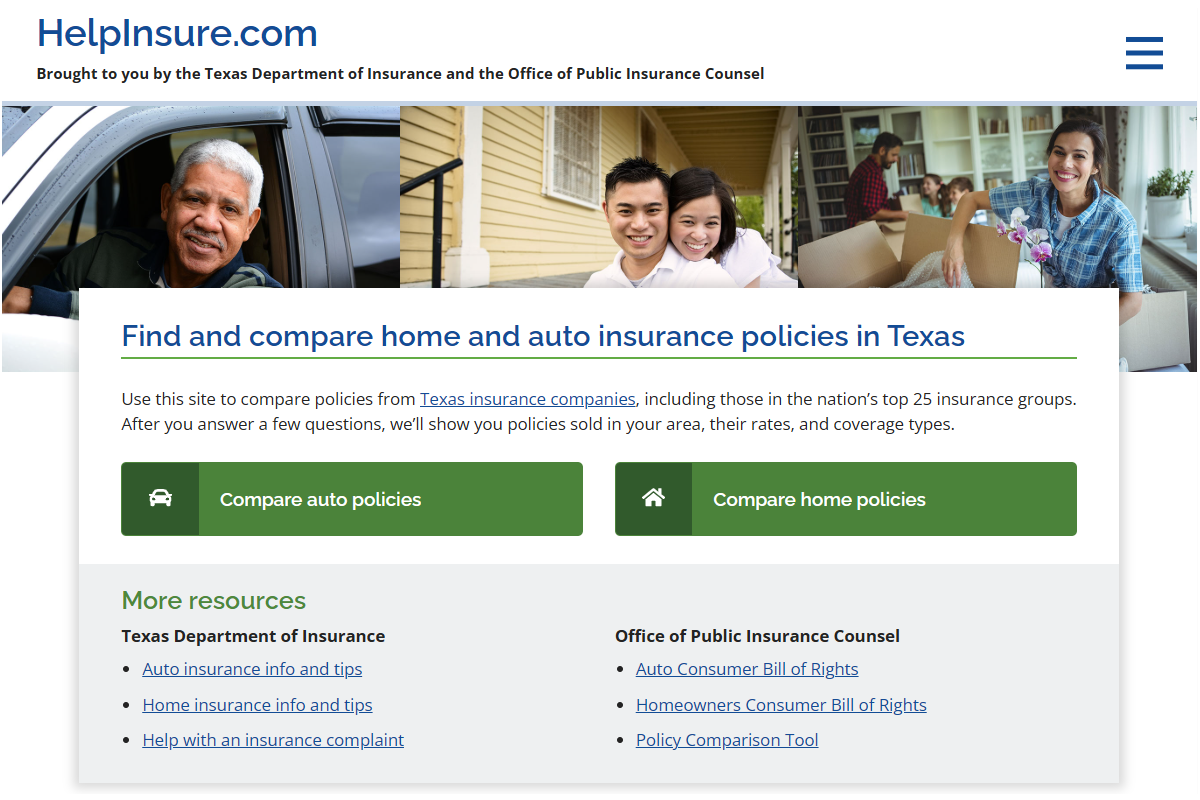

HelpInsure.com helps Texans shop for home and auto insurance

Want a quick list of some home and auto insurance policies sold in your area?

HelpInsure.com is a state-established website where you can search and compare policies from some Texas insurance companies, including the 25 largest insurance groups.

Answer some questions and the site shows policies sold in your area, sample rates, and information on the coverage provided by the policy. You’ll also find a company’s complaint record and financial rating— to help you find the right company.

Once you have your top choices, contact an independent agent or insurance company directly to get actual price quotes. And don’t forget to ask about discounts.

HelpInsure.com is a service of the Texas Department of Insurance and the Office of Public Insurance Counsel.

Have a question about insurance? Call the Texas Department of Insurance at 800-252-3439 or visit www.tdi.texas.gov.

March 2025

Hail damage? Tips to file an insurance claim

Did hail or strong winds damage your home or car?

Your insurance company should pay for hail damage - if you have wind and hail coverage on your homeowners policy or comprehensive coverage on your auto policy.

File a claim quickly.

Other tips for getting paid:

- Take photos or video of the damage. Also, make a list of any damage inside and outside your house or car. Don't throw away damaged items until your insurance company gives permission.

- Prevent more damage. Remove standing water. Cover broken windows and holes to keep out rain. Save all receipts. Your policy may pay for temporary repairs.

- Be available for the adjuster. Make sure the adjuster sees everything.

- Keep a list of everyone you talk to at your insurance company. Be ready to answer questions about the damage.

- Ask about living expenses. If you can’t stay in your house, most policies will cover some related costs. Keep your receipts.

![]()

These columns by the Texas Department of Insurance are available for use in publications. They may be edited as needed and used without copyright. For questions, contact TDI media relations at 512-676-6595 or MediaRelations@tdi.texas.gov.